Introduction: The change that no one wants to accept

The thing is: The global balance of industrial power is not changing – it has changed, and this happened when everyone was busy monitoring politics and arguing over tariffs. China has quietly dominated the major industries that strengthen our present and define the next decade: electric vehicles, solar energy, high-speed rail, shipbuilding, consumer electronics, drones and rare soil processing. If the US wants to compete, it requires a more serious implementation of cable news on low plays and supply chains, depth of manufacturing and commercialisation. This really means that America’s growth will not come from slogans – it will come from the reconstruction of industrial capacity where it is most needed.

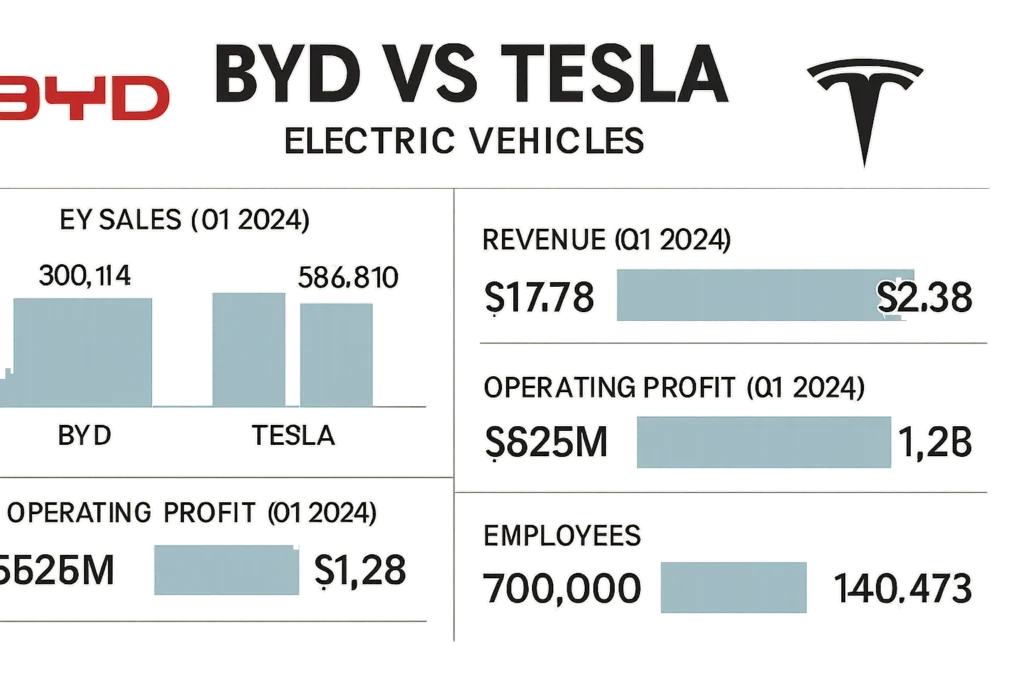

Electric vehicle: Tesla’s crown to BYD machine

Five years ago, no one thought the title BYD would overtake Tesla in global electric vehicle production and sales. With the production of 2024 and the fourth quarter bounce, the Chinese vehicle manufacturer has certainly overtaken Tesla. In 2024, BYD manufactured around 1,777,965 electric vehicles, while Tesla produced 1,774,442, and in the fourth quarter, the difference was about 1,50,000 vehicles.

This pace will continue until 2025

Byd recorded a huge increase in monthly sales. In 2024, the revenue exceeded $ 107 billion and it increased international expansion with aggressive pricing. According to the reports of analysts and transport bodies, the Chinese brands now dominate major ZEV standards and have won more than 50% electric vehicle share in the domestic mixture of major vehicle manufacturers.

The real meaning of this

The real meaning of this is that China’s leading to electric vehicles is no coincidence of subsidy – it is a circle of domestic demand, vertical integration, battery capacity and the speed of reaching the scale. The US is still a leader in software and brand equity, but the factory environment is telling a different story.

Solar Energy: New Oil – and China owns wells

Supply chain control

China controls more than 80% of global capacity in every important phase of the crystalline silicone solar supply chain by China polycylicon, wafers, cells and modules-2023-2026. This is not dominated by “large parts”; This is almost complete control – even in some analyses it has reached 100% in the body and wafer stages.

The scale of investment is shocking

Solar energy invested more than $ 130 billion in 2023 alone, and by 2024, more than 1 TW of wafers/cells/modules capacity will be online, which is sufficient to meet global demand by 2032 in some cases. Between 2020 and the end of 2024, China exported cells and modules worth $ 163 billion, reflecting pricing capacity and supply confidence

Let’s understand this

Let’s understand this: Energy changes run on hardware, and hardware supply chains. China did not succeed only in solar energy manufacturing-it made diversification a geopolitical requirement for everyone else.

High-speed rail: speed, scale and soft power

Network and impact

China’s high-speed rail network is longer than 26,000 miles (more than 40,000 kilometres), leading to a 1,000 km journey in less than five hours. In the meantime, the US is still arguing over permits and corridor rights. This network is not just a domestic facility; It is a platform for rail technology and infrastructure exports in Asia, Africa and Europe.

The thing is

The thing is: High-speed rail (HSR) increases national productivity through regional integration, reliable travel time and labour dynamics-and the benefit of not building to America also gets it. This is an industrial policy with tracks.

Consumer Electronics: Innovation Chakra that no one sees

Ecosystem advantage

Apple’s brand is American, but the rapidly changing innovation pipeline of the wider consumer electronics market lies in the Chinese manufacturing ecosystem that provides major-level features available at large market values. This cycle reduces the time of arrival in the market and accelerates the spread of AI features in middle-level equipment used by billions of people.

The real meaning of this

The real meaning of this is that the centre of “practical innovation” is where the factory, the Palpaza supplier and the assembly lines are located within the same 50 miles – Shenzhen and beyond it. The US still designs chips and platforms, but China converts ideas into fast-paced shipping products.

Ship Building: Control the hulls, shape the flow

Dominance and leverage

About 90% of global trade is carried by ships, and China is now the world’s number one ship manufacturer in all categories, including container ships and tankers, which is ahead of South Korea and Japan, while America proves to be a dwarf. Its impact is the leverage: If a country builds a fleet, it affects standards, maintenance ecosystems and financing networks that operate the maritime economy.

Let us understand this

Let us understand this: Shipping is the blood flow of globalisation – here does not make only jobs; It decides who will take, when, and at what price.

Drone: DJI and 70% reality

Market reliance

According to several industry estimates, DJI has more than 70% of the global citizen drone market, which is used in cinematography, agriculture, inspection and even defence-related applications. Despite safety concerns, American agencies and contractors have also found themselves dependent on Chinese platforms due to cost and capacity.

Its real meaning is that

Its real meaning is that China did not make only drones; it also created standard kits for air robotics in various industries – default hardware for the sky filled with functionality.

Rare Earth: Calm Ostructive Points

Processing power

From China’s smartphones and EV motors to fighter aircraft and missile guidance, about 90% of the world’s rare earth elements used in everything are processed. Mining is one thing; The real strength lies in processing, and China is the lord of the middle stage where raw ore becomes a strategic input.

The thing is

The thing is: Processing is not attractive, but it is full of profit and practice. Until the refineries and separation facilities outside China, the technical sovereignty will remain a hope, not a plan.

Fee vs. Supply Series: Where America is lagging behind

Structural issues

Analysts say the fees may slow down the pace of a competitor, but they do not rebuild domestic manufacturing, supplier density or logistics efficiency-which are the necessary forces for victory in hardware-intensive areas. The American CEO ran after the cost and speed towards China for decades as the Chinese system provided both.

Dilemma

Dilemma: America benefited from cheap and fast supply chains abroad, and the memory of domestic production weakened. To reverse it, there is a need to be patient, predictive policy and bend towards construction instead of buying.

What can America do – now

Choose the area and go to the depth

Choose the area and go to the depth: battery, grid hardware, power electronics, advanced packaging and industrial robotics are high-leverage bets where talent, intellectual property and demand already exist.

Construct the supply chains from beginning to end

Construct the supply chains from beginning to end: raw materials, midstream processing, component construction, final combination – no tight missed.

Practice “boring excellence”

Practice “boring excellence”: permission correction corresponding to factory needs, port modernisation, standardisation and building professional pipelines.

Use demand to increase supply

Use demand to increase supply: Federal/state procurement and incentives of PTC/ITC-style that reward not only the installation, but also the domestic capacity and learning process.

Be honest about the cost

Be honest about the cost: Risoring is a national capacity project-expect the price hike in the starts, then reduce it with the scale and construction-for-design.

Implementable workbook for American builders and policymakers

- Battery and cathode/anode supply lines: co-place processing with cell plants; Ensure long-term lift with miners; Invest in domestic graphite/silicone anode and LFP/LMFP cathode lines.

- Grid Hardware Blitz: Transformer, switchgear, inverter – federal/state procurement guarantee and extending domestic manufacturing supported by streamlined location determination.

- Rail and logistics modernisation: focus on high-throughput corridors and doubling the goods rail digitisation; Evaluate regional HSR pilots where passengers and margins exist.

- Marine Industrial base: Encourage the American shipyard for containers and tanker construction; Create financing vehicles according to the terms of Asian shipbuilders.

- Drone Industrial Strategy: Support modular, safe, American-made airframe and payload ecosystem; Purchase mass for agriculture, inspection, disaster response.

- Rare soil and significant minerals: Mid-stream separation/refinement and financed to magnet factories; Create stores with community benefits and speed up environmental reviews.

For entrepreneurs and operators

- EV ecosystem: Software-defined vehicle layers, charging analysis, battery health markets and second-life battery platforms, riding on the EV scale curve regardless of the brand.

- Solar/storage services: operation and maintenance for distributed assets, inverter repair and fleet management; Supply of hedging tools to EPC affected by module/inverter instability.

- Drone services: Data-e-Saravis for agriculture, utilities and construction; Regulatory navigation tools for flight permissions and compliance reporting.

- Industrial Material: Practical training library for factory technicians and energy installers associated with certification and employer partnership.

Major dataable data

- Revenue of BYD 2024: approximately $ 107.2 billion; Sales will continue to increase rapidly in 2025.

- Fast in China EV shares: Chinese vehicle manufacturer in ZEV rankings dominates; BYD overtook Tesla in BEV sales in 2024.

- Solar Supply Series: Polysilicon, Wafer, Sale, China in Module Capacity> 80%, 2023-26 forecast.

- PV exports: Solar PV cell/module exports from China between January 2020 to September 2024.

- Byd vs Tesla 2024 EV Production: 1,777,965 vs 1,774,442; Byd ahead of 150,000 by a margin of fourth quarter.

Story Sutra: Why China’s strategy was effective – and how to compete

China chose areas whose effects grow together – battery, solar energy, transport hardware – and made such a large scale that it re -re-established global pricing and standards. This paired the policy certainty with harsh implementation, strengthening the domestic demand as the final trench.

The US can still win in system integration, software, chip design and leading research and development – but only when it is associated with factories that can turn the designs at reality at competitive costs and speeds. Without this, the US continues to write the script while someone else takes direction, shooting, editing and box office.

Has BYD really overtaken Tesla?

Yes. Several datasets confirm that BYD overtook Tesla in global BEV sales in 2024, it would continue to speed up in 2025 and will also increase EV production in total, which reflects a structural change rather than a one-time quarter of one time.

Can America get away from solar energy without a huge rise in prices?

Diversification is happening, but China still controls more than 80% of the PV supply chain in the mid-decade. At the beginning of any rapid change will be higher costs until the expansion and vertical integration of the non-sugar capacity is done.

If China is a leader in manufacturing, where can the US lead?

In chip design, advanced software, grid orchestration, industrial automation and system integration – these powers are re-recombined with domestic manufacturing and midstream processing to avoid strategic obstacles.

Conclusions: Compete where necessary

Power comes after generation. China did not gain overnight – it has been achieved through the depth of manufacturing, scale economy and disciplined implementation in the most important hardware categories of the 21st century. The US can also match him, but he will again have to think like a manufacturer: choose the path, go to the depth, capture the middle part, and expand continuously.